Section 206AB or 206CCA Alert!!! Non-filers of ITR – TDS or TCS to be deducted at double rates. Recently I came across a Notice from CAMS, wherein a notice was received by Investor, specifying that the PAN of investor is appearing in a list of “Specified Persons” as per Income Tax Utility and as a consequence deduction of TDS will be done at higher rate on all dividend payouts. This article is guide on what is Section 206AB or 206CCA, impact of Section 206AB or 206CCA, how to do compliance and how to check the list of specified persons.

These sections are clear indication of intentions of our Tax Authorities in India and emphasis on “Importance of Income Tax Return filing and timely return filing”. The Taxpayers have to ensure filing of their returns within due date of Section 139(1) year on year.

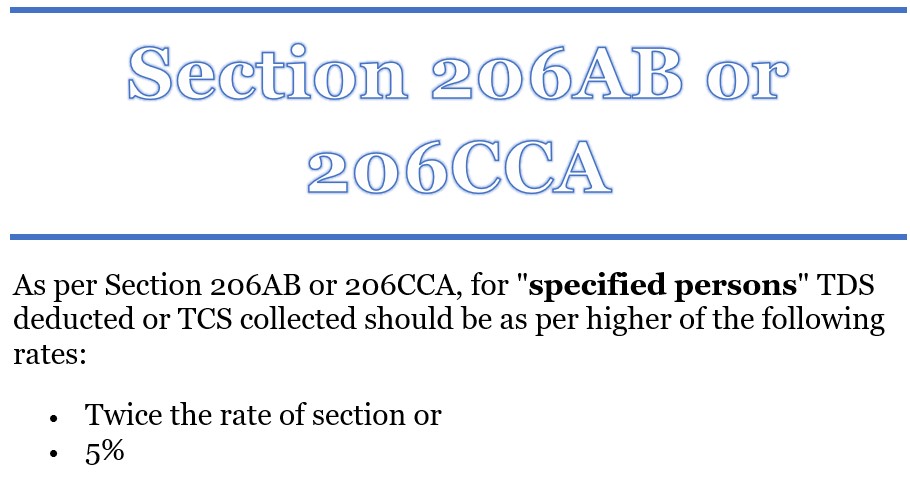

What is Section 206AB or 206CCA of Income Tax?

On which TDS section this Section 206AB or 206CCA is not applicable

- 192

- 192A

- 194B

- 194BB

- 194IA

- 194IB

- 194LBC

- 194M

- 194N

Specified Person as per Section 206AB or 206CCA?

A specified person will be as one falling in all of the below categories :

- Person whose aggregate of Tax deducted at source and Tax collected at source exceed INR 50,000 in a year and return of income for that year was not filed within the time limit of section 139(1).

- Person can be resident or non resident but does not include non resident who does not have permanent establishment in India.

Impact of Section 206AB or 206CCA

As per CBDT Circular dated 17 May, 2022 following key impacts of the section are:-

- For F.Y. 2022-23, a list will be made at the beginning of year and will be available on reporting portal. Specified persons means assessee who has not filed return of income for F.Y 2020-21 till the end of assessment year A.Y. 2021-22. If the return is filed for F.Y. 2021-22, the name will be removed from list of F.Y 2023-24. The name can be also removed if aggregate of TDS and TCS does not exceed 50,000 in F.Y. 2021-22.

- The list will be updated only once, so all the tax collectors and deductor have to just check the reporting portal once for list of specified persons.

- However, if TDS/TCS returns are revised for F.Y. 2021-22 and aggregate of TDS and TCS does not exceed 50,000 in F.Y. 2021-22, then the list will be updated.

- If section 206AA, wherein PAN is not furnished or incorrect PAN is furnished by deductee, higher of the 2 rates will be applicable i.e. as per 206AB or 206AA.

Procedure to check list of specified persons under Section 206AB or 206CCA

- Logon to income tax portal using TAN based login. If the same is not yet registered same can be registered using TAN number.

- Go to Tab “Pending Actions”

- Select Reporting Portal from the drop down.

- Register yourself on Reporting portal by selecting option “New Registration”

- Select form “Compliance Check – Tax deductor and Collector”

- Add the Principal officer/owner details.

- The application will be approved and login credentials will be shared on registered email ID.

- The password has to updated.

- The users can search PAN individually or using Bulk PAN search option to check whether person covered in specified person list.

For further details on registration on reporting portal refer >> https://report.insight.gov.in/reporting-webapp/portal/homePage

Notice received for deduction of tax at higher rates? Reach out to our experts at TaxLedgerAdvisor

For expert assistance on Notice received for deduction of tax at higher rates in Udaipur and Rajasthan, reach our professionals at Tax Ledger Advisor.

Also refer other articles on TDS from TaxLedgerAdvisor

https://taxledgeradvisor.com/tds-u-s-194ia/

https://taxledgeradvisor.com/section-194-r-deduction-of-tax-on-benefit-or-perquisite/